What the Recovery Means for Buyers and Homeowners in Lee and Collier Counties

Southwest Florida homeowners insurance looks very different in 2026 than it did two years ago. Insurance companies are competing for Florida homeowners again. Carriers had spent several years leaving the state, going insolvent, or refusing new policies. Now the market has turned. Premiums are flattening, and capacity is returning, which means more insurers are willing to write policies and take on Florida risk. Whether you are buying a home or reviewing the policy on a home you already own, that change reframes the math on a major cost of ownership. This guide covers where the market stands, which carriers are driving the recovery, and how to estimate your insurance costs.

With local insurance perspective from Jenna Adams, Private Client Advisor, Marsh McLennan Agency, Fort Myers.

Key Takeaways

- More than 17 carriers have entered Florida since the 2022 and 2023 reforms. Average requested rate increases have dropped from nearly 22% two years ago to under 1%.

- Inland and newer homes are seeing the most relief. High-exposure coastal and waterfront properties can still face steep renewals.

- Roof age remains one of the biggest drivers of insurability. Florida law protects many roofs from age-only nonrenewal. Older asphalt shingle roofs still get close scrutiny.

- Standard homeowners policies generally address wind damage. Flooding from storm surge or rising water requires separate coverage.

- Florida’s free CHOICES tool lets buyers compare sample rates by county. Real quotes also depend on the home and the buyer’s own insurance history, so treat the tool as a directional estimate.

How Southwest Florida Homeowners Insurance Reached a Breaking Point

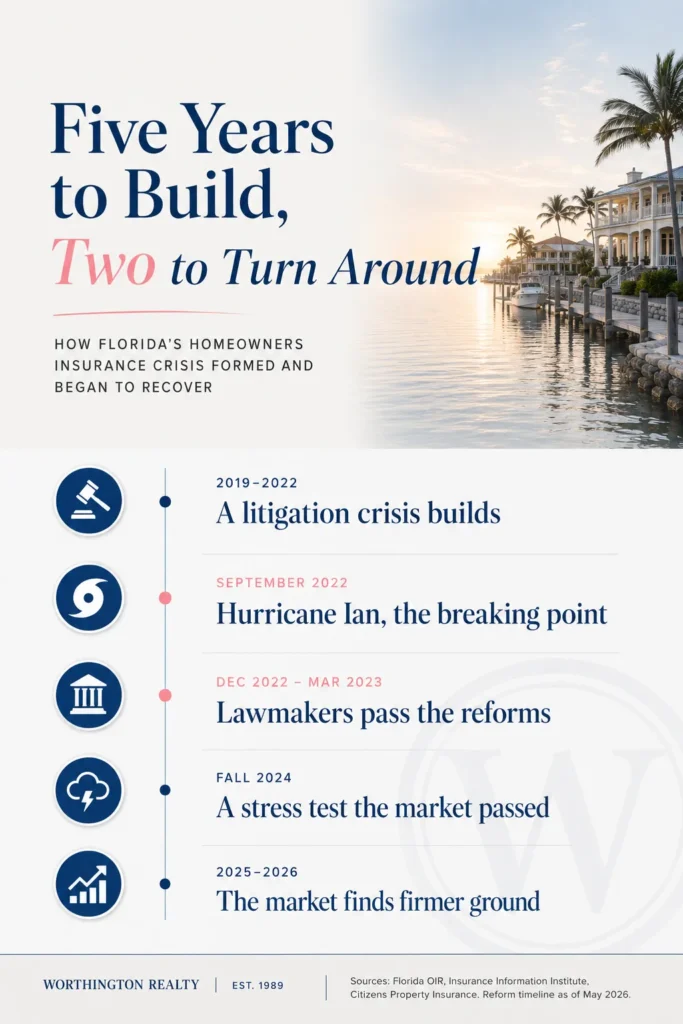

Florida’s insurance crisis took five years to build. Hurricanes set the baseline cost of insuring a coastal state, but litigation is what pushed the market toward collapse, and litigation is what the reforms set out to fix.

A Crisis Built on Lawsuits

Florida’s insurance trouble built through 2019 to 2022, driven primarily by litigation. In 2020, Florida had only about 9% of the nation’s homeowner insurance claims. Yet it generated close to 79% of the nation’s homeowner insurance lawsuits. That imbalance drove insurer losses to unsustainable levels. Carriers responded by raising rates, restricting new business, or leaving the state entirely. Six insurers became insolvent in 2022 alone, and more than a dozen others either exited or stopped writing new policies.

Two features of Florida law explain how the litigation grew. The first was a “one-way attorney fee” rule. A policyholder who sued an insurer and won any amount, even a single dollar, had their legal fees paid by the insurer. The insurer recovered nothing if it prevailed. The second was the Assignment of Benefits agreement, which let a homeowner sign their claim rights over to a contractor. Together, these two rules created an opening. A contractor could take over a claim, submit invoices that insurers frequently challenged as excessive, and sue the insurer at little financial risk if it pushed back. Both rules began as consumer protections. The combination turned routine claims into a litigation pipeline. The legislature narrowed the practices in 2019 and closed them more fully with the 2022 and 2023 reforms.

Hurricane Ian and the Breaking Point

Hurricane Ian made landfall near Fort Myers and Cape Coral as a Category 4 storm in September 2022. It became the costliest hurricane in state history at more than $112 billion in damage. Ian pushed an already fragile market past its breaking point. United Property & Casualty, one of the larger carriers in the region, was declared insolvent the following February.

The Reforms That Turned It Around

The turning point came in December 2022, when the state enacted Senate Bill 2-A. House Bill 837 followed in March 2023. Together these reforms ended the one-way attorney fee structure and the assignment-of-benefits practices. Regulators and insurers had widely cited both as major drivers of litigation. Hurricanes Helene and Milton struck the region in the fall of 2024, and the market absorbed those losses without a new wave of insolvencies. The carrier collapses had clustered around Ian in 2022. By the time the 2024 storms arrived, the reforms had already taken hold.

Carriers Are Coming Back

Carrier filings and state approvals show the recovery in Southwest Florida homeowners insurance most directly. Florida’s Office of Insurance Regulation reports that more than 17 property and casualty insurers have entered the market since the reforms. The approvals ran steadily into 2025, with recent entrants including Viceroy Preferred Insurance, the Orion180 companies, and Texas-based Incline National. Companies do not apply to write business in a market they expect to keep losing money in.

Established national carriers have also re-engaged. Nationwide returned to the Florida homeowners market. Heritage resumed writing new policies in August 2024 after a period of restricted appetite.

Premiums Are Flattening, and Starting to Fall

Rate filings tell the same story from a different angle. The OIR reports that the 30-day average requested rate change for homeowners came in around 0.8%. Two years earlier, that figure was 21.8%. Florida posted roughly a 1% average homeowners rate increase in 2024, the smallest since 2019. Citizens Property Insurance is the state-backed insurer of last resort. It has now filed its first rate decrease in a decade, an average cut of about 2.6% for personal lines.

The insurer’s own numbers make the recovery concrete. Citizens’ policy count peaked near 1.42 million in October 2023. By early 2026 it had fallen to roughly 336,000, a drop of about 76%. That decline was partly engineered. Under a 2022 law, a Citizens customer who receives a private-market offer within 20% of their Citizens premium loses eligibility to stay, so much of the shrinkage came from policies being moved to private carriers rather than homeowners choosing to leave. The mechanism still signals a real recovery, because private carriers only make those offers when they are willing to take on Florida risk.

Two things are worth keeping in mind. First, statewide improvement does not mean every Southwest Florida ZIP code sees the same thing. Whether a given carrier will write your home still depends on roof age, home value, claims history, and proximity to water. Second, homeowners moved out of Citizens through depopulation sometimes saw their premium rise at the next renewal. If you were part of a takeout, have your coverage reviewed rather than assuming the new policy is automatically a better deal.

Insurance Is Now Part of the Buying Decision

For a buyer, insurance has become a real part of evaluating a home, on the same level as inspection and financing. As you search for homes across Southwest Florida, a few principles make the process smoother.

Estimate Insurance Before You Offer

Estimate insurance before you make an offer, not at closing. A new owner generally cannot assume the prior owner’s policy. The seller’s premium is only a rough guide to yours.

Treat Roof Age as a Central Factor

Florida law gives homeowners real protection on roof age. An insurer cannot refuse to write or renew a policy solely because of roof age if the roof is under 15 years old. For older roofs, a homeowner-paid inspection showing at least five years of useful life keeps the policy in force. Carriers still scrutinize older roofs closely, especially asphalt shingle roofs. They may require an inspection, documentation, or replacement if the roof has limited life left.

Here Ian left an unexpected mark on the region. The storm forced roof replacements across entire neighborhoods of Lee and Collier counties. As a result, a large share of homes on the market today have roofs only three or four years old. Many of those sellers are sitting on an insurability advantage they may not know how to point to. A buyer comparing two similar homes should ask about roof age early.

Budget Wind and Flood Together

Treat homeowners coverage and flood coverage as one combined number. Standard homeowners policies generally address wind damage. They do not cover flooding from storm surge or rising water. Flood is a separate policy through the National Flood Insurance Program or a private carrier. The exposure is real: FEMA estimates that a single inch of floodwater can cause up to $25,000 in damage. In coastal and low-elevation parts of Lee and Collier counties, flood coverage is a meaningful line item rather than an afterthought.

Compare Carriers Before You Commit

Plan to compare carriers rather than accept the first quote. Each company prices roof age, water distance, and claims history on its own model. The same home can produce very different premiums depending on who writes it.

A Free Tool to Estimate Insurance Costs: Florida’s CHOICES Database

Most homeowners do not know CHOICES exists. It is the official rate-comparison tool published by the Florida Office of Insurance Regulation at choices.floir.gov/pandc/homeowners. It shows sample premiums from carriers writing in your county, drawn from the most recent rate filings approved by the state.

Running the Tool Takes About a Minute

The tool offers three preset home profiles. Two are a $150,000 pre-2001 home, shown with and without wind mitigation, which lets you see what mitigation alone is worth. The third is a $300,000 newer-construction home. You pick a profile, choose your county, and the tool returns a ranked list of carriers with sample annual rates.

The Same Home, Very Different Prices

The numbers only help if you know how to read them. A Lee County run for the $300,000 new-construction example, checked in May 2026, returned 20 carriers. The spread was striking, from roughly $3,000 at the low end to more than $38,000 at the top. Because the tool reflects the most recent approved filings, the exact figures move over time, but the pattern holds. A few notes turn that into a useful picture:

- The two cheapest results were USAA companies, which only write for military-affiliated households. For the general public, the realistic floor was Citizens at about $3,933. A cluster of Florida Farm Bureau and State Farm Florida followed near $4,100.

- The mid-tier names, including TypTap, Monarch, Heritage, Homeowners Choice, and Slide, represent much of the working Southwest Florida market today.

- The two highest figures, well above $30,000, were high-net-worth and surplus-lines carriers built for large coastal estate homes. They are not a realistic comparison for a typical $300,000 house. Set them aside when you read the range.

Used with that context, CHOICES is a credible, government-sourced way to ground your expectations before you contact an agent. It is an estimate rather than a quote. A carrier’s actual eligibility and pricing depend on the specific home and on the buyer. Your insurance score, prior claims, and payment history all affect the rate a carrier offers, and the sample profiles cannot account for any of that. Even so, it tells you what a competitive premium looks like and how wide the field really is.

Insuring High-End and Coastal Homes in Southwest Florida

Jenna Adams, Private Client Advisor at Marsh McLennan Agency in Fort Myers, shares where higher-end and coastal buyers still run into friction:

“Higher-end coastal homes are often insured through high-net-worth carriers like PURE or Chubb, but those policies come with conditions: minimum insured values, square footage and elevation requirements, distance-to-coast limits, and often a requirement to bundle other coverage like auto or excess liability. Elevation matters even for spaces below the main living area. A garage where someone stores a collector or exotic vehicle sits lower, so a buyer should ask what it costs to insure that vehicle in a special flood hazard zone, or to store it inland instead.

On the construction side, an elevated frame home, especially on a barrier island, usually carries more risk than concrete block, so any wind mitigation credits you can add will lower the premium for years. And always look at flood alongside homeowners. Ask whether the current owner has a flood policy, because it can often be assumed by the buyer and grandfathered into the existing rating. That holds for both National Flood Insurance Program policies and some private ones.”

Frequently Asked Questions

Premiums are flattening and, in some cases, declining. The average requested homeowners rate change has fallen from over 21% two years ago to under 1%. Citizens has also filed its first rate decrease in a decade. Southwest Florida homeowners insurance is improving, though the relief is uneven and depends on the individual home.

More than 17 carriers have entered the Florida market since the 2022 and 2023 reforms. Established carriers including Nationwide and Heritage have re-engaged as well, and Florida-based carriers like Frontline have become increasingly competitive in Southwest Florida through independent agencies. Whether a specific carrier will write your home depends on your ZIP code, roof age, home value, and claims history. A local agent or broker who shops multiple carriers is the most reliable way to know who is actively writing in your area.

Start with Florida’s free CHOICES tool at choices.floir.gov/pandc/homeowners, which shows sample rates by county. For an accurate quote, work with an insurance agent or broker who shops multiple carriers, knows which ones write in your ZIP code, matches your home to the right underwriters, and spots gaps between wind and flood coverage.

No. Standard homeowners policies cover wind damage but exclude flooding from storm surge or rising water. Flood coverage requires a separate policy through the National Flood Insurance Program or a private flood carrier. In coastal Southwest Florida, budgeting homeowners and flood coverage together gives you an accurate picture of total cost.

Each carrier prices risk on its own model. They weigh roof age, distance to water, flood zone, and claims history differently. A single Lee County home profile can produce premiums ranging by a factor of three or more across carriers. That is why comparing several quotes, rather than accepting the first one, is worth the effort.

The Bottom Line for Southwest Florida

The Florida insurance market looks materially healthier than it did two years ago. Some Southwest Florida coastal areas still see volatile pricing. Carriers are returning, rate increases have nearly stopped, and Citizens is shrinking back toward its intended role as a safety net. The market now offers more options and steadier pricing than it has in years.

If you already own a home here, this is a good time to have your coverage reviewed, especially if a takeout moved you off Citizens. If you are buying, treat insurance as part of the search itself, not a closing-day surprise. Price it early, ask about roof age, and factor it into what a home truly costs to own. When you are ready to start, browse homes for sale across Southwest Florida, and talk with a Worthington Realty agent who can help you weigh insurance alongside everything else that goes into the right purchase.